Overcoming Obstacles to Buyouts

What are the three biggest obstacles preventing property buyouts from working effectively? I submit they are 1) timeliness, 2) funding for low- and middle-income families, and 3) the inability of low-income homeowners to find comparable housing. The three issues often come into play at the same time, making buyouts even less successful.

Let’s talk about the issue of timeliness. After a disaster, many of those who experienced significant damage are receptive to a buyout since they know they will be flooded again. If they have flood insurance, they hope the insurance will pay a significant share of the cost of rebuilding. However, if their home was substantially damaged (more than 50% of its value) they have to meet the current local floodplain management standards, which require elevation or demolition. In older, lower income neighborhoods, homes may have been built long before the National Flood Insurance Program (NFIP) or any state or local development standards for flooding existed. That could mean their first floor was well below the base flood elevation (1% chance flood level) and now must be elevated at or above the flood protection elevation to comply. That may add more than $100,000 to the repair costs. Understandably, many low- and middle-income folks simply cannot afford that additional cost.

Wait a minute, there is a provision of the flood insurance policy that helps offset the added costs to comply with the new standards. The problem is, it won’t cover that $100,000 cost — it may provide up to $30,000 and it is not always available as the law says it should. For many years, ASFPM has promoted raising Increased Cost of Compliance (ICC) coverage to at least $90,000 and making it available in all the ways the law says. FEMA has proposed changing the law to provide up to 20% of insured value, which may work for high-value homes. However, that can still create problems for lower income residents. If a home is only insured for $50,000, that means only $10,000 is available for mitigation. The proposed language must be modified. To see more on ASFPM recommendations to modify ICC and other provisions see our detailed priorities for NFIP reform.

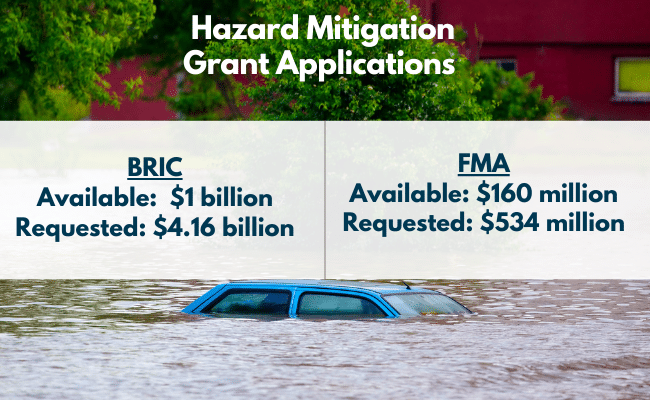

Now let’s say the homeowner is asked by the community to volunteer for a buyout as part of a FEMA mitigation grant. That should address the matter, right? Unfortunately, no. Now enters the timeliness issue along with the equity issue. Despite attempts to expedite the process, the average time for a FEMA mitigation grant remains 4-5 years. Forcing someone who has just flooded to suffer through 4-5 years of indecision and uncertainty is simply cruel. Higher income folks may be able to rent another home, a motel, or have other options for housing during the long period of time. Lower income homeowners often do minimal fixes to the house just so they have a place to live for the next couple years. But after a couple years they give up, do what they can to fix up the home or even worse, walk away from the home with no compensation. Mitigation experts across the nation agree that these long timelines are the primary deterrent to wider acceptance and success with mitigation.

How do we overcome the timeliness issue? Experience has shown that mitigation grants can actually occur within 6-12 months. The key is a strong state program that works with the community to get its mitigation plan together before a disaster occurs — we know where natural disasters like floods and hurricanes are likely to happen and who will be impacted when they do. Having a community plan ready and homeowners educated enables the grant to move ahead quickly.

What can we do to help the homeowner find comparable housing? There is actually a federal standard for federal buyout and relocation programs to consider those participants “displaced persons.” Under the law, the federal agency must then utilize the Uniform Relocation Act (URA), which provides added funding to help them find comparable housing. Most federal agencies like HUD, USACE, etc. use the URA, but FEMA has sought to avoid the URA by claiming the buyouts are voluntary, and the URA does not apply. In addition, FEMA has a process to provide additional funding when no comparable housing is available, but those in the field tell us this creates a heavy burden in terms of documentation and approval, and also lengthens an already arduous timeline. It appears some added direction is needed here.

Some of these issues require upgrades in the law, but others only require the locals and state to be organized and have a plan in place before disaster strikes. If you have ideas for other ways buyouts can be better accomplished, please share with me at larry@floods.org

As we were putting the finishing touches on this column, The New York Times published an in-depth article on post-disaster housing issues and the impact on people in Lake Charles, Louisiana. Read How the Government Is Failing Americans Uprooted by Calamity.