Rethinking Relocation Assistance for More Equitable Outcomes

Last week, while attending the National Association of Flood and Stormwater Management Agencies meeting, I listened to FEMA leadership talk about the new FEMA strategic plan, which has as its first goal: Instill equity as a foundation of emergency management. FEMA explains the need to focus on equity in this way:

Underserved communities, as well as specific identity groups, often suffer disproportionately from disasters. As a result, disasters worsen inequities already present in society. This cycle compounds the challenges faced by these communities and increases their risk to future disasters. By instilling equity as a foundation of emergency management and striving to meet the unique needs of underserved communities, the emergency management community can work to break this cycle and build a more resilient nation.

When I think about the delivery of FEMA’s hazard mitigation programs, I wonder if we could make these programs more equitable by doing more to assist with relocation assistance for acquisition projects?

Here is the idea.

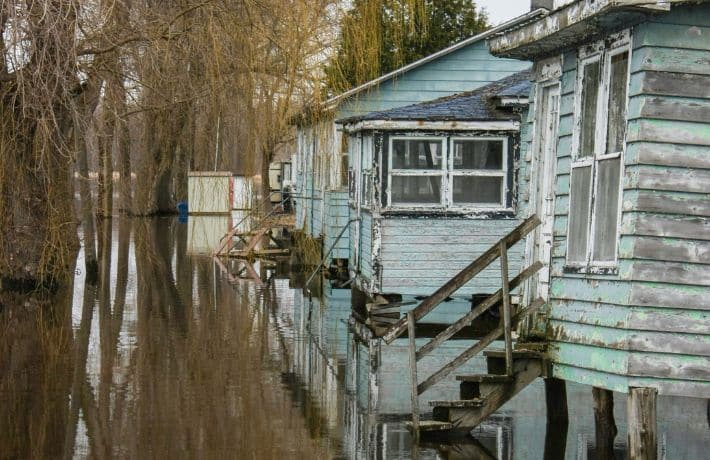

Earlier in my career as a State Hazard Mitigation Officer, I was often frustrated by the inability to provide much additional relocation assistance beyond the limited amount allowed by FEMA policy, which was in lieu of what could be provided under Uniform Relocation Assistance (URA). The argument made for not providing more assistance was that buyouts were voluntary and therefore didn’t trigger the requirements for URA.

Here’s why that’s a flawed argument and why I think URA is necessary. Relocation assistance payments are intended to ensure that individuals who experience significant flood damage to their property are able to relocate to a comparable, safe, and sanitary replacement dwelling outside the floodplain or hazard area. The problem I experienced as a SHMO, and so many others continue to experience, was that I dealt with many property owners who were not only lower income, but also had very low value homes. So the result of the policy was that the assistance in lieu of URA was not enough, but when URA was triggered (and there were instances where URA could be triggered, such as renters displaced when trying to acquire mobile homes or mobile home parks), it made the benefit-cost analysis impossible to overcome.

One way to solve this problem would require two adjustments to current policy. The first would be to more fully take advantage of URA by triggering it for property owners that were living in the home, even though buyouts would continue to be voluntary. In that way, the full array of URA-type assistance could be provided and it would be much more likely than not to help people relocate to decent, safe, and comparable housing. A second approach would be to exempt URA assistance, perhaps as well as other assistance needed to comply with other federal or state housing, health, and safety requirements, from benefit-cost analysis. The philosophical reason is that these are not costs related to the physical act of reducing flood risk; rather, they are costs that are a result of federal laws where society as-a-whole benefits. A similar argument could be made for costs related to either asbestos abatement or underground storage tank remediation. Any of these situations can add so much cost during benefit-cost analysis that it can make it impossible to proceed with the home acquisition, leaving folks in harm’s way. And although anecdotal and based on my personal experience, it seems that the homes with the majority of problems like asbestos siding are in lower income communities and neighborhoods —perhaps because the owners never had the means to fix the problems in the first place.

Some have suggested that we get rid of benefit-cost analysis altogether. I am not so sure this is a good idea, as there does need to be some basis to determine how to prioritize funding since demand is so much greater than available resources for flood mitigation. However, in order for this idea to work, both policy adjustments need to be made. It would be a mistake to simply allow or trigger more URA funding without also changing how it is handled as part of benefit-cost analysis. Otherwise, you very well could have the unintended consequence of limiting mitigation for more people and property where equity is already an issue.

One encouraging piece of legislation in this regard is HR 7842, which would not only result in a novel way to do expedited buyouts if an insured, repetitive or severe repetitive loss property was substantially damaged and would have otherwise made an insurance claim to the full claim limit; but also would automatically deem participants in the Hazard Mitigation Grant Program as “displaced persons” for the purposes of the Uniform Relocation Act, thereby triggering the full array of potential URA resources available.

The idea for this column began forming while I was sitting in an airport trying to get home from the NAFSMA meeting after a canceled flight. There are many possibilities for rethinking the programs that we as floodplain and hazard mitigation managers work with every day to make them more just and equitable. This is one idea among many that I am sure are out there, and I look forward to working with FEMA and other agencies that ASFPM works with to make the necessary policy adjustments to result in the better delivery of federal programs to those that need them.

Your partner in loss reduction,

Chad